While struggling with debt isn’t uncommon, getting out of it as soon as possible is important. Student loans, car loans, credit cards and other payments can lead to your pile of debt getting bigger and bigger. So, what steps should you take if you are in debt? Keep reading to find out.

1. Clean Out Your House & Sell What You Don’t Use

Start small and simply sell the things you don’t need. You’d be surprised how many things you have around the house that you never use. While doing this won’t erase your debt, it will give you some extra money to put towards paying it off and help you recognize some of the unnecessary purchases you’ve made.

2. Find a Side Job

If you have a full-time job but have weekends open, finding a part-time job to fill that time would be extremely beneficial. Working on your days off might not seem ideal, but if you’re serious about paying off your debt, it’s a great step in the right direction. Just remember these circumstances are temporary and the bigger your steps towards erasing your debt are, the quicker you can get it done.

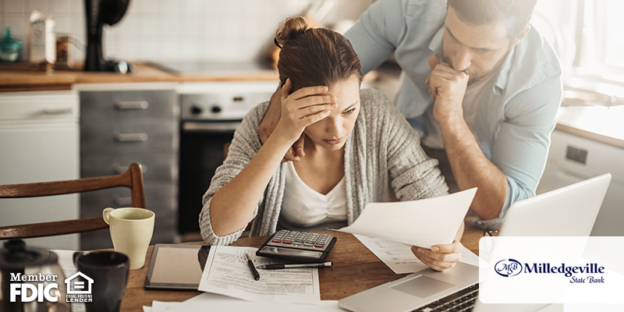

3. Analyze Your Spending Habits

The best way to understand your spending habits is to write all of your payments from the last month or two down on paper. Once you see everything in front of you, try dividing that into categories – necessary expenses (like rent, utilities, groceries, etc.) and unnecessary expenses (coffee trips, clothes, video games, etc.). Now that you see how much you’ve spend on things that aren’t necessary, start rethinking the way you handle your money every day. Next time you think of buying that cute shirt, ask yourself if you need it. These small purchases add up and the money could be put towards your debt, instead!

4. Never Spend More Than You Make

How do people get into debt? They spend more money than they’re bringing in. If you’re trying to get rid of debt, you definitely can’t be adding more money to that pile. Trim down your budget so you know you’re making more than you’re spending. The best way to know if you’re doing this is to simply track everything you spend and everything you make. At the end of your pay period, make sure the money earned is higher than the money spent.

Paying off the debt you owe might seem like a big job, but freedom from debt starts with taking the first step. Start by implementing these effective tips into your daily life, stay organized and keep a positive mindset. Debt is temporary if you work hard and stay motivated! Get saving by opening a savings account with us today.